It’s been a while since we discussed workers’ comp requirements, not only here in Florida but nationwide. This requirement for all employers is often misunderstood.

It’s been a while since we discussed workers’ comp requirements, not only here in Florida but nationwide. This requirement for all employers is often misunderstood.

We still find business owners with no coverage telling us “I’m exempt.” After further review we often find that it’s not what they think …

Where Did Workers’ Comp Come From?

The history of worker’s comp goes back thousands of years. Apparently it was discussed on some tablets discovered from Sumeria around 2050 BC, where workers could be compensated if they lost fingers, toes or other extremities. It was first established by a law in Prussia in 1871, by then Chancellor Otto von Bismarck 1. While largely a political move, it did set significant legal precedents.

Although many US states started passing individual laws as early as 1908, it wasn’t a national requirement until 1972, and then supported by the American Disabilities Act (ADA) of 19732. It is still largely controlled by individual states.

What is Workers’ Comp?

Simply put, any employer in the United States is required to compensate an employee who is injured on the job. While there are many, many exceptions, this is true the majority of the time. Since we are a Florida based company, we will be referring to Chapter 440 of the Florida Statutes from here on quite a bit.

The second paragraph of the FL law states:

“440.015 Legislative intent.—It is the intent of the Legislature that the Workers’ Compensation Law be interpreted so as to assure the quick and efficient delivery of disability and medical benefits to an injured worker and to facilitate the worker’s return to gainful reemployment at a reasonable cost to the employer….”

This is a good working definition.

So Who is Required to Have Workers’ Comp?

First let’s rephrase this. All Employers are subject to the comp laws. Yes. If you are an employer, and one of your employees gets hurt in the normal course of daily duties, you the Employer are responsible for all medical expenses, administrative expenses (includes legal fees) and two-thirds of lost wages. The definitions are in chapter 440.02, which we will be dipping in and out of as this article goes on.

In short, all employers are required to “have” workers’ comp. The trick comes in defining what “have workers’ comp” means.

Most states require employers to have a policy in place, with minimum limits, from an admitted carrier in the state of residence. One notable exemption is the state of Texas, which does not require a policy, although it is strongly encouraged.

It is important to note that even if you don’t have a policy from an admitted carrier, you are still responsible for workers’ comp for your employees. You are in essence, self insured.

So I’m Not Exempt Automatically?

Very few employers are automatically exempt. Some employees are automatically exempt, see 440.02(15)(VII). Here is a partial list of automatically exempt employees, or exempt types of employment:

- A licensed real estate agent

- Domestic servants in private homes

- Certain agricultural laborers

- Professional athletes for qualifying pro sports teams

- Prisoners and sentenced laborers

- Musicians and members of performing groups under temporary contract

Notice that there is no automatic exemption for “less than a certain number of employees.” We see this quite often. While it is true that you may not be required to have a policy, you are in reality just self insured, as you are still responsible for any and all expenses related to an employee injury. 440.02(15)(b) defines those people eligible for an exemption. The exemption must be applied for. In non-construction industries it is free. Otherwise there is an annual fee.

Also, in Florida, if there is one other employee besides the employer in a Construction Industry, a policy is required. An exemption is not available.

What is a Construction Industry?

Let’s see what 440.02 has to say about it

440.02(8) “Construction industry” means for-profit activities involving any building, clearing, filling, excavation, or substantial improvement in the size or use of any structure or the appearance of any land.

Notice that this includes all home service industries such as lawn cutting, painting, pool service, pest control, plumbing, handyman, electrician, etc.

Local Story

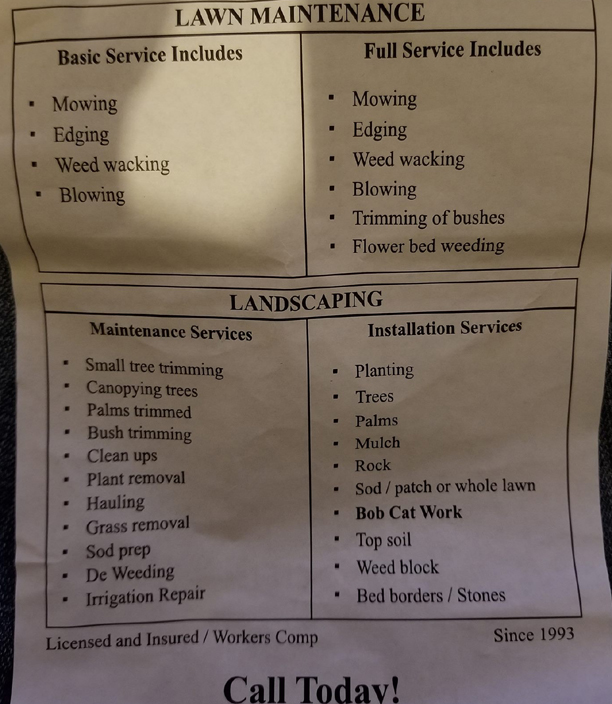

Recently a lawn cutting company distributed fliers in various neighborhoods looking for work. The flier boldly claimed: “Licensed and Insured / Workers’ Comp”. We contacted the company and asked for proof of insurance. They sent us a copy of their non-construction exemption. They also told us they had two employees in addition to the owner. There are several things wrong with this:

Recently a lawn cutting company distributed fliers in various neighborhoods looking for work. The flier boldly claimed: “Licensed and Insured / Workers’ Comp”. We contacted the company and asked for proof of insurance. They sent us a copy of their non-construction exemption. They also told us they had two employees in addition to the owner. There are several things wrong with this:

First, they probably deceived the state. The state asks if they are a construction industry and they checked the “no” box. Perhaps they didn’t understand the law but still, that’s no excuse.

Second, they may have deceived the consumers. They do not have a workers’ comp insurance policy. They are self insured. You may ask, as a homeowner, “why do I care if they workers’ comp or not?” It is a valid question. Here’s why. In several cases, employees were injured while working on a homeowner’s property. The contractor was “exempt”. The attorneys hired by the injured workers sued the homeowner’s insurance policy for coverage. Even though the policy does not require them to pay this claim, in most cases a significant settlement was reached to avoid costs of defense, and the ensuing year the homeowner’s insurance rates went up or they were cancelled for “underwriting reasons.”

Third, they didn’t understand the law. This combination of deception and ignorance should be a very large warning sign to the consumer. The first warning sign was the very low price they extended for services. Yes, the price might be cheaper than someone doing it ethically and legally, but look at the possible costs.

Please don’t ask us for the name of the contractor. They are in the process of correcting the errors they made.

Is There More We Need to Know?

Plenty! But enough for this week. We’ll continue this series in the weeks to come.

1Worker’s Compensation in the United States

2A Brief History of Workers’ Comp